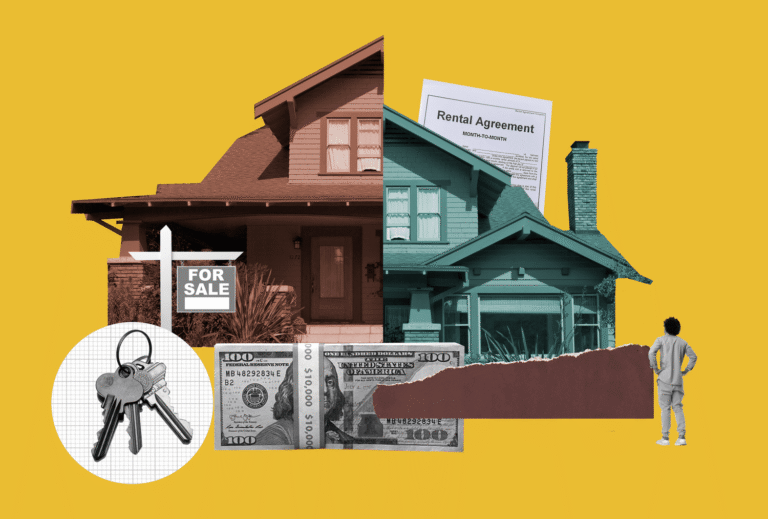

For many aspiring homeowners, the dream of buying a house can feel out of reach—especially when faced with saving for a large down payment or qualifying for a mortgage. This is where rent-to-own homes present a practical and flexible solution. With a rent-to-own agreement, renters can live in a home now with the option to purchase it later. This gives them valuable time to build credit, save money, or simply get a feel for the property and neighborhood before committing to ownership.

In today’s competitive housing market, rent-to-own arrangements can offer a real advantage. They provide an alternative path to homeownership for individuals who may not be financially ready to buy outright but are working toward that goal.

In this guide, we’ll break down how rent-to-own homes work, what buyers need to know before entering an agreement, and the key benefits and drawbacks to keep in mind. We’ll also cover the legal aspects and offer tips to help ensure your experience is smooth and informed. Whether you’re working to improve your financial standing or just want more flexibility in the home-buying process, rent-to-own could be the strategic step forward you’ve been looking for.

How Rent-to-Own Homes Work

Some of your monthly rent may go toward the purchase price. That means you’re slowly building equity while renting. This makes it easier to transition into ownership when you’re ready.

Look for rent-to-own listings online or talk to a local real estate agent experienced in these deals. Want to learn more? Read NerdWallet’s rent-to-own guide

.

Pros and Cons of Rent-to-Own Homes

Pros: One of the biggest benefits of choosing to rent-to-own a home is the ability to lock in a purchase price. This can be especially advantageous in rising markets. Buyers can live in the property while building their credit and saving for a down payment. Some agreements allow a portion of the rent to be applied toward the future purchase, giving renters the opportunity to build equity gradually. This arrangement also provides time to decide whether the home and neighborhood truly fit your lifestyle.

Cons: The biggest risk is losing the option fee and any rent credits if you decide not to—or can’t—buy the home. Additionally, the purchase price is typically agreed upon upfront, which could work against you if home values decline. Maintenance responsibilities are often passed to the tenant, so it’s crucial to clarify those expectations before signing.

Legal and financial complexities are another drawback. Many rent-to-own contracts are not standardized, which makes them harder to enforce or navigate without professional guidance. That’s why working with an experienced

real estate lawyer is highly recommended.

Learn more about these agreements from: Investopedia’s rent-to-own breakdown.

Who Should Consider Rent-to-Own Homes?

Rent-to-own homes can be an excellent option for buyers who face challenges qualifying for traditional mortgages. This includes individuals with lower credit scores, limited savings for a down payment, or those who need time to improve their financial situation. By choosing to rent-to-own a home, buyers gain the opportunity to build credit and save while already living in their future property.

First-time homebuyers often benefit from rent-to-own arrangements as they offer a less intimidating entry point into homeownership. Additionally, those relocating to new areas may find this model appealing because it gives them time to settle in and assess the neighborhood before fully committing.

However, rent-to-own isn’t ideal for everyone. Buyers must be financially disciplined to avoid losing their upfront option fee and rent credits. They also need to be confident about purchasing the home when the lease ends. Rent-to-own agreements typically require a strong commitment, and backing out can lead to financial losses.

If you’re considering this path, consult resources such as our

Rent-to-Own Home Buyers Guide for detailed advice. It’s also wise to discuss your situation with a

mortgage specialist who can help you understand your financing options.

Understanding your readiness and financial goals will help determine if a rent-to-own home is the right choice for you in today’s market.

Benefits of Rent-to-Own for Buyers

Rent-to-own homes offer several advantages, especially for buyers who may not be ready for a traditional mortgage. One of the biggest benefits is the ability to lock in a purchase price early. This can protect buyers from rising home prices in competitive markets, giving them peace of mind as they work toward homeownership.

Another advantage is the opportunity to build credit and save for a down payment while living in the home. Since part of the rent is often credited toward the eventual purchase, buyers accumulate equity over time. This can make it easier to qualify for a mortgage when the lease ends.

Rent-to-own arrangements also provide flexibility. Buyers can test living in a neighborhood before fully committing to the purchase. This “try before you buy” approach helps ensure the home and location meet their needs.

Additionally, rent-to-own can be a good option for those with less-than-perfect credit or limited savings. It allows time to improve financial standing without losing out on the chance to secure a home.

To learn more about how to make the most of a rent-to-own agreement, visit our

Rent-to-Own Tips for Buyers page. If you’re curious about market trends, check out our Real Estate Market Updates.

Final Thoughts on Rent-to-Own Homes: Is It Right for You?

Rent-to-own homes present an intriguing option for buyers who may not yet be ready or able to secure traditional financing but want to work toward homeownership. This arrangement provides a unique opportunity to lock in a purchase price, build equity through monthly payments, and improve credit or save for a down payment during the rental period. It can be especially appealing in competitive or rapidly appreciating markets where locking in a price early can protect against rising costs.

However, it’s important to approach rent-to-own agreements with caution. Buyers need to carefully review contract terms to understand their responsibilities, such as maintenance obligations and the conditions required to exercise the purchase option. The financial commitment, including upfront option fees and potentially higher rents, should be weighed against the benefits. Additionally, buyers must have a clear plan for securing mortgage financing at the end of the lease period to avoid losing their investment.

For sellers, rent-to-own offers a way to attract committed tenants and potentially achieve a higher sale price, but it also carries risks if the buyer does not ultimately purchase the property.

In summary, rent-to-own homes can be a valuable pathway to homeownership for those who qualify, but due diligence is essential. We recommend consulting real estate professionals and legal experts to ensure the agreement is fair and aligns with your long-term goals.

For further details, visit our comprehensive guide on Rent-to-Own Homes and explore how this alternative approach can fit your unique circumstances.